Dear Patron,

Capitalism has been the most productive economic system over the last century. This is mainly due to the efficient allocation of resources (Labour, Capital) as they move from unprofitable/less profitable industries to the more profitable ones. This leads to a spurt of competition in industries offering long-term growth potential and high return profile. While competition leads to innovation and affordable prices, it also disrupts the environment for the incumbents in the near-term. However, it is important to avoid painting every scenario with the same brush as higher competition can also have a positive impact on the incumbents in the long-term. It has been observed that in many instances, new entrants have in-fact expanded the market but eventually fallen by the bay. This has helped the large incumbents to take their share in a much bigger market. Entry of Patanjali helped in expanding the ayurveda market, which benefitted players such as Dabur, HUL etc.

Several industries such as paints, diagnostics have seen heightened competition recently, leading to sharp correction in stock prices. While markets can be irrational in the near-term, it reflects the fundamentals in the long-term. In this newsletter, we will deep dive to analyse the impact of new entrants across sectors.

1. FMCG

Indian FMCG market is estimated to be over USD 100 billion and can be broadly divided into 3 categories – (1) Food and beverages (F&B) (2) Beauty and personal care (BPC) (3) Home care. The industry is dominated by MNC such as HUL, Reckitt Benckiser , P&G, Nestle and home grown companies like Dabur, Emami, Adani-Wilmar and Marico.

In its 45th AGM, Reliance Industries Ltd announced that its retail arm – Reliance Retail – is foraying into the FMCG industry by taking its private-label FMCG brands, currently sold at its supermarkets (Reliance Fresh, Reliance Smart) to general trade (Refer Exhibit: 1). Reliance Retail has 15,866 stores with an area of 45.5 million sq ft and a turnover of ~Rs2 lakh crore for the FY21, a scale unparalleled in the Indian retail industry. Entry of such a large player with deep pockets has send shock waves across the industry.

Reliance is looking to leverage JioMart’s network of 2mn+ retailers and appointment of super stockists. Isha Ambani also stated their plans on increasing their distribution reach. "We are on course to partner with one crore merchants, as we expand our presence to cover the entire country, serving over 7,500 towns and 5 lakh villages in the next five years,"

Exhibit 1: Reliance already has a large number of private label brands across categories

Source: Ambit Asset Management

Our Take:

FMCG companies have 3 key competitive advantages – Brand, Distribution, and Scale. Out of the 3 key competitive advantages, Reliance scores well in Scale, average in Distribution and weak in Brands.

Brand is a significant moat in F&B and BPC categories, where consumer involvement is very high. Consumers are hesitant to try unknown brands that can jeopardize their health. In order to scale packaged foods and BPC categories, we believe Reliance will have to acquire smaller brands. It is currently in talks to acquire brands such as Garden Namkeens from CavinKare, besides other brands such as Lahori Zeera and Bindu Beverages. Reliance also acquired soft drink brand Campa from Pure Drinks Group in a deal estimated at Rs 22 crore.

While Reliance already has a pan India network of stores, building offline distribution will still be a challenging task. Strong brand pull is critical for retailers to provide any shelf space. This is a chicken and egg story where distribution requires strong brand pull and brand pull can be created only once the company has a loyal customer base. We see offline scalability only in staple foods and home care segments due to limited consumer involvement, fragmented players, use of pricing as a lever, etc. Contrary to the initial expectations, Reliance has struggled in jewellery and footwear industry. Existing players like Titan, Metro continue to do well in spite of years of RIL’s presence and decent aggression in advertising spends.

The FMCG category has strong global players who have had decades of experience fighting in a competitive marketplace. These companies have talent, resources, R&D and scale. Companies such as Nestle, ITC are operating at a massive scale with strong brands and extensive distribution network. Therefore, we believe that higher competitive intensity will have a limited impact on the incumbents.

2. Diagnostics

Diagnostics industry is ~Rs70k Cr market, largely dominated by hospitals (37%) and Standalone Centres (46%) (Refer Exhibit). Diagnostic chains account for only 17% market share with top 4 players accounting for mere ~5% market share. Highly fragmented nature of the industry presents a good opportunity for the organised chains to grow. Diagnostic chains have grown faster than the overall industry with mid-teens sales CAGR in last 5 years.

Exhibit 2: Standalone Diagnostics centre stand to be more vulnerable to increasing competition

Source: Vijaya Diagnostics RHP, Metropolis RHP, CRISIL Research, Ambit Asset Management

Diagnostic industry offers strong return profile, low capital investment and is expected to grow at 10-12% CAGR led by several structural factors. These benefits coupled with increased health awareness post COVID have led to an influx of entrants – online aggregators, hospital chains, pharma companies, and pharmacy chains. Challengers are differentiating with new age tech, aggressive pricing, and bundled offerings.

Some of the new entrants include:

- Tata acquired pharmacy 1MG and launched its own diagnostics operation

- Reliance acquired e-pharmacy Netmeds to grow its diagnostic arm

- PharmEasy acquired Thyrocare

- Medplus (pharmacy retailer) started diagnostic operations in Hyderabad

- Large hospital chains such as Aster DM, Max Hospitals

- Pharmaceutical companies such as Lupin, Mankind, Torrent group

Influx of companies has increased the concerns regarding the growth and profitability of large incumbents. This was reflected in the sharp decline in their stock price in last 6 months. While this may give a sense that leaders may lose their turf, a few factors stand out –

Lower penetration offers ample room for market expansion – Diagnostics is still underpenetrated in india. Top-20 Cities still account for >50% market size. This is where majority of the new competition is coming up. The large untapped market presents huge scope of expansion, especially in Tier-2/3/4 cities. Players such as Dr Lal, which has a strong hub-spoke model, can benefit by expanding the existing clusters.

Fragmented market share – Market share of the top players in India accounts for only ~5%. Compare this with other larger countries like US, Brazil Indonesia where the largest players have 20-30% market share. Larger, organized players in our view have lot of room to grow provided they can work on their (1) Execution (2) Scale up of acquisitions (4) Cost Leadership

Game of Scale – Thyrocare is the perfect example of using scale and volume to offer the lowest cost proposition and in turn gain market share. It processes >10k samples per day and therefore is able to offer competitive pricing. Scale can act as a significant competitive advantage against the new entrants.

Brand: The industry has gone through a long period of transformation. From being a doctor driven industry, it has slowly pivoted to a more consumer-centric industry where brands have started to play an important role. This shift was accentuated by COVID when people become more conscious of their health. Post covid, customers are choosing known brands, which provide reliable reports and higher convenience.

3. Paints

Flood of new entrants – Paints, a 60000 cr industry, has seen tremendous increase in competition in the recent past. Strong long-term growth visibility and superior return profile has attracted several players. Grasim Industries announced plans to invest 10,000 crore for its paint foray by FY25 which would result in a production capacity of 1,332 million litres per annum. This has jolted the entire industry as the capacity addition is ~40% of the cumulative capacity of top 4 players. Also, Grasim can leverage its already established distribution network of 54k dealers in white cement business, out of which 70% are present in the paints.

In addition to the same, Astral acquired 51% stake in Gem Paints for Rs. 194 crore. Similarly, Infra.Market invested 270 crore in Shalimar Paints through a combination of equity and debentures. JK Cement has also announced a foray into paints with an investment of around 600 crores. All of the above signifies intense competition in the Industry.

Brand and Distribution are key Moats – In decorative paints (75% of overall industry), Brand (higher consumer involvement in paints) and Distribution remain the key competitive advantages. Brand salience is much higher in metro/tier1 compared to smaller towns, where dealers have higher influence. Also, Asian paints is able to supply paints to dealers within 3-6hrs, while other companies take 12-24hrs. Creating strong brands and distribution network is a time consuming process and cannot be achieved by committing higher capex.

Difficult to disrupt the leaders – Market leaders such as Asian Paints were able to deter competition and continued to gain market share despite all the efforts by some of the largest global paints companies. In the past, we have seen similar level of competition from Sherwin Williams, Jotun, Du Pont, BASF, Valspar and Sigma Kalon. Most of the mentioned players have either exited or could not gain any substantial market share. The inability of the larger entrants such as Sherwin Williams and Jotun to gain market share was primarily due to low capital investment (~200-300 crores), inability to expand their distribution network and unsuccessful brand building.

While the competition this time have committed large capital which may disrupt the industry, we believe building brand and distribution network will require continuous investments for a prolonged period of time. Large players have sheer scale and size of distribution and have built brands over several decades, both of which are extremely difficult to replicate.

4. Insurance

India is likely to become the sixth largest insurance market in the world in the next 10 years, supported by regulatory underway and the rapid economic expansion. Tech enabled insurers (Insurtech) have enabled innovation across the insurance value chain. They have been able to personalise both the product offering and customer servicing. They are also offering products based on demographics, customer needs at various life stages, individual behaviour and preferences, and real-time interaction. Players such as Acko and Digit are gaining market share in niche categories which are underserved by current players.

Acko has partnered with cab aggregator Ola to offer insurance for taxi rides, which is seeing significant traction. Digit's smartphone protection policy not only covers damage to phones but also offers pickup and drop facilities for phone repair. Digit is also working on products like pet insurance, where pets can be covered against health expenses incurred at veterinary clinics. The company has tied up with Cleartrip to insure passengers against delayed and missed connecting flights as well.

Key competitive advantages in Insurance industry are – Scale and distribution. Despite the entry of a large number of digital insurers such as Go digit and Acko, the insurance sector is still dominated by the private banca backed insurers. HDFC Life and ICICI Prudential Life succeeded more due to the distribution strength of HDFC and ICICI Bank. Max Life has benefited from its distribution deal with Axis Bank. Several early entrants such as Aviva India, Future Generali, Exide Insurance etc are still struggling to attain significant size despite being in the market for over 15 years. Therefore, we feel gaining higher traction for new InsureTech players will not be an easy ask.

CONCLUSION:

The main goal of any business is to deliver profitable growth. Industries which offer strong growth potential with superior return profile will always witness phases of heightened competition. There are times when new entrants have displaced the incumbents by addressing a gap in the market. Discount brokers such as Zerodha, Upstox and Angel have disrupted the brokerage industry by no frills offering at discounted prices. However, there are times when new competition haven’t been able to gain any meaningful market share.

Similar concerns were raised in 2018, when Aditya Birla Fashion and Retail Ltd (ABFRL) entered the inner wear segment with its brand – Van Heusen. Entry of a large player coupled with subdued revenue growth of Page Industries, led to a sharp correction in Page’s stock price. We at Ambit believed in the franchise when the street turned negative. We had a few key insights which helped us ride this difficult, yet rewarding journey. Firstly, it is hard to gain share in inner wear category due to high customer loyalty (comfort/fit remains critical). Also, expanding distribution network is a difficult and long exercise. ABFRL gave higher credit/margin to distributors and was successful in offloading inventory initially. However, even after getting favourable terms, distributors and retailers made subpar ROI as the retail offtake remained slow. Even operating at much higher scale, Page has been able to double its retail network (50k to 110k) during the same time. Therefore, while Van Heusen has done well in the outer wear segment, it still hasn’t been able to scale meaningfully in the inner wear segment.

Exhibit 3: Page Industries has delivered decent returns despite volatility…

Source: Ambit Asset Management, Bloomberg

Exhibit 4: …and during that volatility, the company maintained margins and OCF growth / conversion

| Rs. Cr. | FY17 | FY18 | FY19 | FY20 | FY21 | FY22 |

|---|---|---|---|---|---|---|

| Sales | 2,130 | 2,552 | 2,852 | 2,946 | 2,833 | 3,887 |

| YoY Gr. | 20% | 12% | 3% | -4% | 37% | |

| EBITDA | 413 | 541 | 617 | 533 | 527 | 785 |

| % Margin | 19% | 21% | 22% | 18% | 19% | 20% |

| CFO | 274 | 455 | 230 | 517 | 696 | 327 |

| Capex | 61 | 56 | 37 | 74 | 14 | 98 |

| FCFF | 212 | 398 | 192 | 442 | 683 | 229 |

Source: Ambit Asset Management

Therefore, it is important to analyse whether the competition is addressing gaps in the market and has right to win (capital investment, execution capabilities, etc). At Ambit, we believe that players such as Nestle, Asian Paints, Dr. Lal Pathlabs have significant competitive advantages in their respective industries. While we feel new entrants have committed large capital, they are not addressing any significant gap in the market offering, yet. Therefore, higher competition poses limited threat for the incumbents over the long-term.

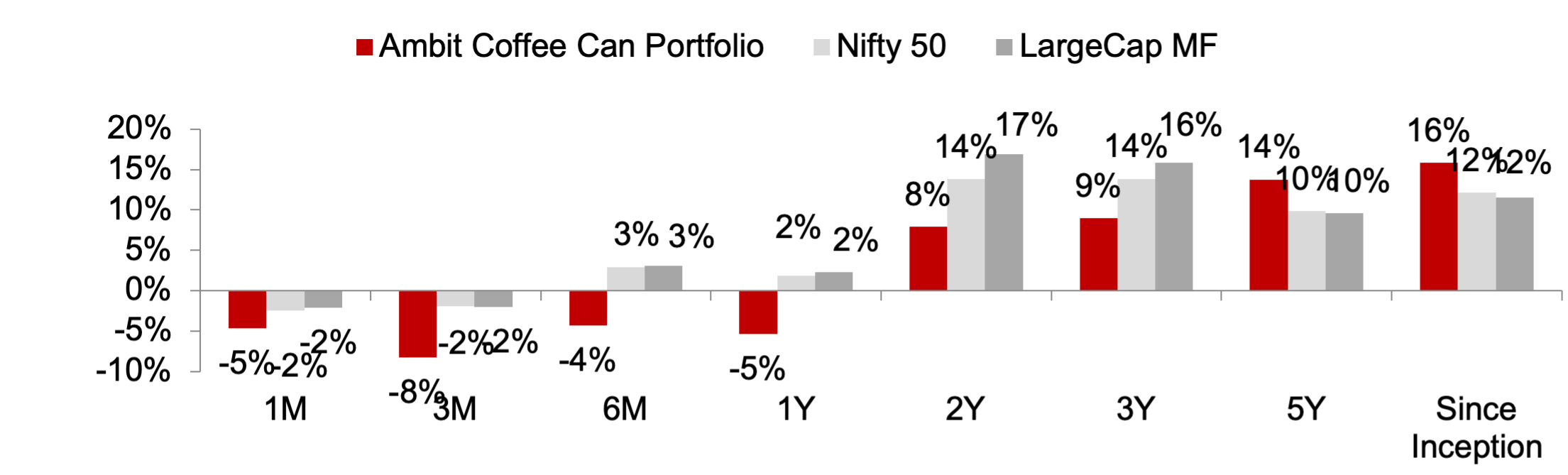

Ambit Coffee Can Portfolio

At Coffee Can Portfolio, we do not attempt to time commodity/investment cycles or political outcomes and prefer resilient franchises in the retail and consumption-oriented sectors. The Coffee Can philosophy has unwavering commitment to companies that have consistently sustained their competitive advantages in core businesses despite being faced by disruptions at regular intervals. As the industry evolves or is faced by disruptions, these competitive advantages enable such companies to grow their market shares and deliver long-term earnings growth.

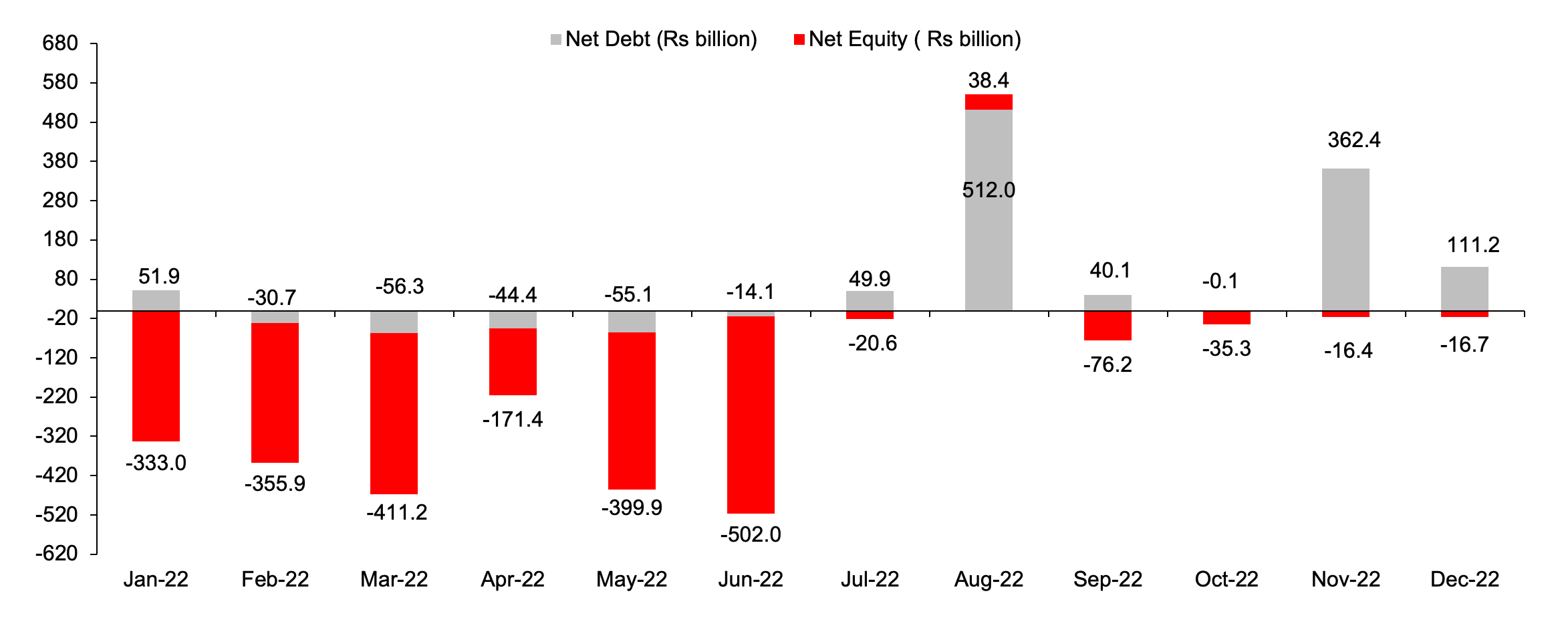

Exhibit 5: Ambit’s Coffee Can Portfolio point-to-point performance

Source: Ambit; Portfolio inception date is March 6, 2017; Returns as of 30th September, 2022; All returns are post fees and expenses; Returns above 1-year are annualized; Note: Returns prior to Apr’19 are returns of all the Pool accounts excluding non-aligned portfolio, and returns post Apr’19 is based on TWRR returns of all the pool accounts.

Exhibit 6: Ambit’s Coffee Can Portfolio calendar year performance

Source: Ambit; Portfolio inception date is March 6, 2017; Returns as of 30th September; All returns are post fees and expenses. Note: Returns prior to Apr’19 are returns of all the Pool accounts excluding non-aligned portfolio, and returns post Apr’19 is based on TWRR returns of all the pool accounts.

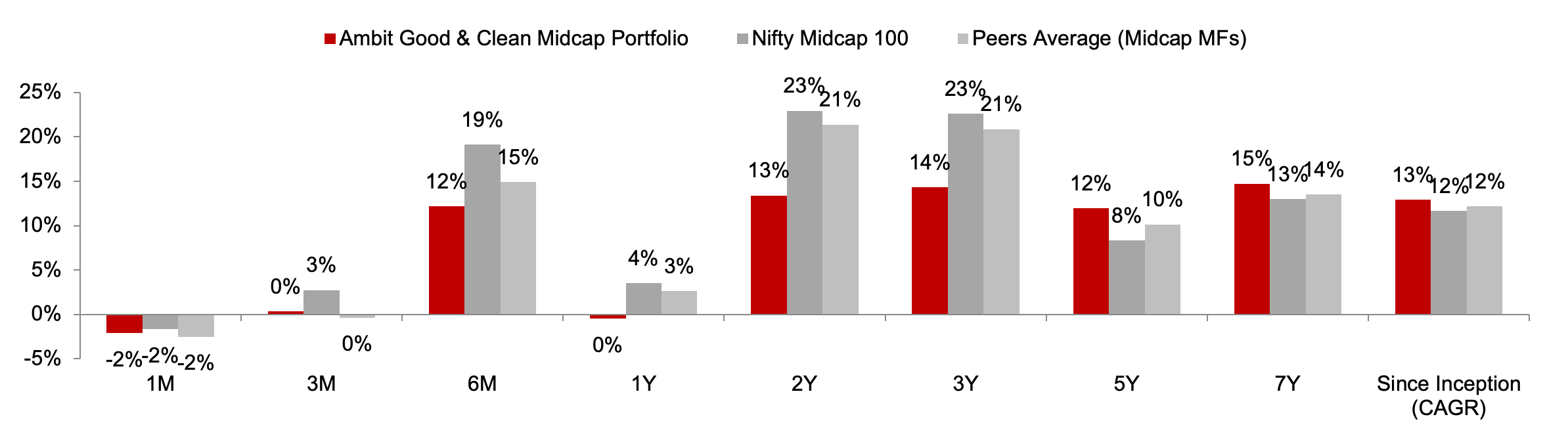

Ambit Good & Clean Midcap Portfolio

Ambit's Good & Clean strategy provides long-only equity exposure to Indian businesses that have an impeccable track record of clean accounting, good governance, and efficient capital allocation. Ambit’s proprietary ‘forensic accounting’ framework helps weed out firms with poor quality accounts, while our proprietary ‘greatness’ framework helps identify efficient capital allocators with a holistic approach for consistent growth. Our focus has been to deliver superior risk-adjusted returns with as much focus on lower portfolio drawdown as on return generation. Some salient features of the Good & Clean strategy are as follows:

- Process-oriented approach to investing: Typically starting at the largest 500 Indian companies, Ambit's proprietary frameworks for assessing accounting quality and efficacy of capital allocation help narrow down the investible universe to a much smaller subset. This shorter universe is then evaluated on bottom-up fundamentals to create a concentrated portfolio of no more than 20 companies at any time.

- Long-term horizon and low churn: Our holding horizons for investee companies are 3-5 years and even longer with annual churn not exceeding 15-20% in a year. The long-term orientation essentially means investing in companies that have the potential to sustainably compound earnings, with this compounding earnings acting as the primary driver of investment returns over long periods.

- Low drawdowns: The focus on clean accounting and governance, prudent capital allocation, and structural earnings compounding allow participation in long-term return generation while also ensuring low drawdowns in periods of equity market declines.

Exhibit 7: Ambit’s Good & Clean Midcap Portfolio point-to-point performance

Source: Ambit; Portfolio inception date is March 12, 2015; Returns as of 30th September; All returns above 1 year are annualized. Returns are net of all fees and expenses

Exhibit 8: Ambit’s Good & Clean Midcap Portfolio calendar year performance

Source: Ambit; Portfolio inception date is March 12, 2015; 30th September. Returns are net of all fees and expenses

Ambit Emerging Giants Portfolio

Smallcaps with secular growth, superior return ratios and no leverage –Ambit's Emerging Giants portfolio aims to invest in small-cap companies with market-dominating franchises and a track record of clean accounting, governance and capital allocation. The fund typically invests in companies with market caps less than Rs4,000cr. These companies have excellent financial track records, superior underlying fundamentals (high RoCE, low debt) and ability to deliver healthy earnings growth over long periods of time. However, given their smaller sizes, these companies are not well discovered, owing to lower institutional holdings and lower analyst coverage. Rigorous framework-based screening coupled with extensive bottom-up due diligence lead us to a concentrated portfolio of 15-16 emerging giants.

Exhibit 9: Ambit Emerging Giants Portfolio point-to-point performance

Source: Ambit; Portfolio inception date is December 1, 2017; Returns as of 30th September; All returns above 1 year are annualized. Returns are net of all fees and expenses

Exhibit 10: Ambit Emerging Giants Portfolio calendar year performance

Source: Ambit; Portfolio inception date is December 1, 2017; Returns as of 30th September. Returns are net of all fees and expenses

Ambit TenX Portfolio

Ambit TenX Portfolio gives investors an opportunity to participate in the India growth story as the Indian GDP heads towards a US$10tn mark over the next 12-15 years. Mid and Small corporates are expected to be the key beneficiaries of this growth. The portfolio intends to capitalize on this opportunity by identifying and investing in primarily mid & small cap companies that can grow their earnings 10x over the same period implying 18-21% CAGR. Key features of this portfolio would be as follow:

- Longer-term approach with a concentrated portfolio: Ideal investment duration of >5 years with 15-20 stocks.

- Key driving factors: Low penetration, strong leadership, light balance sheet

- Forward-looking approach: Relying less on historical performance and more on future potential while not deviating away from the Good & Clean philosophy.

- No Key-man risk: Process is the Fund Manager

Exhibit 11: Ambit TenX Portfolio point-to-point performance

Source: Ambit; Portfolio inception date is December 13, 2021; Returns as of 30th September; Returns are net of all fees and expenses

Exhibit 12: Ambit TenX Portfolio calendar year performance

Source: Ambit; Portfolio inception date is December 13, 2021; Returns as of 30th September. Returns are net of all fees and expenses

For any queries, please contact:

Umang Shah- Phone: +91 22 6623 3281, Email - [email protected] | Ambit Investment Advisors Private Limited - Ambit House, 449, Senapati Bapat Marg, Lower Parel, Mumbai - 400 013

Risk Disclosure & Disclaimer

The performance of the Portfolio Manager has not been approved or recommended by SEBI nor SEBI certifies the accuracy or adequacy of the performance related information contained therein. Ambit Investment Advisors Private Limited (“Ambit”), is a registered Portfolio Manager with Securities and Exchange Board of India vide registration number INP000005059.

This presentation / newsletter / report is strictly for information and illustrative purposes only and should not be considered to be an offer, or solicitation of an offer, to buy or sell any securities or to enter into any Portfolio Management agreements. This presentation / newsletter / report is prepared by Ambit strictly for the specified audience and is not intended for distribution to public and is not to be disseminated or circulated to any other party outside of the intended purpose. This presentation / newsletter / report may contain confidential or proprietary information and no part of this presentation / newsletter / report may be reproduced in any form without its prior written consent to Ambit. All opinions, figures, charts/graphs, estimates and data included in this presentation / newsletter / report is subject to change without notice. This document is not for public distribution and if you receive a copy of this presentation / newsletter / report and you are not the intended recipient, you should destroy this immediately. Any dissemination, copying or circulation of this communication in any form is strictly prohibited. This material should not be circulated in countries where restrictions exist on soliciting business from potential clients residing in such countries. Recipients of this material should inform themselves about and observe any such restrictions. Recipients shall be solely liable for any liability incurred by them in this regard and will indemnify Ambit for any liability it may incur in this respect.

Neither Ambit nor any of their respective affiliates or representatives make any express or implied representation or warranty as to the adequacy or accuracy of the statistical data or factual statement concerning India or its economy or make any representation as to the accuracy, completeness, reasonableness or sufficiency of any of the information contained in the presentation / newsletter / report herein, or in the case of projections, as to their attainability or the accuracy or completeness of the assumptions from which they are derived, and it is expected each prospective investor will pursue its own independent due diligence. In preparing this presentation / newsletter / report, Ambit has relied upon and assumed, without independent verification, the accuracy and completeness of information available from public sources. Accordingly, neither Ambit nor any of its affiliates, shareholders, directors, employees, agents or advisors shall be liable for any loss or damage (direct or indirect) suffered as a result of reliance upon any statements contained in, or any omission from this presentation / newsletter / report and any such liability is expressly disclaimed. Further, the information contained in this presentation / newsletter / report has not been verified by SEBI.

You are expected to take into consideration all the risk factors including financial conditions, risk-return profile, tax consequences, etc. You understand that the past performance or name of the portfolio or any similar product do not in any manner indicate surety of performance of such product or portfolio in future. You further understand that all such products are subject to various market risks, settlement risks, economical risks, political risks, business risks, and financial risks etc. and there is no assurance or guarantee that the objectives of any of the strategies of such product or portfolio will be achieved. You are expected to thoroughly go through the terms of the arrangements / agreements and understand in detail the risk-return profile of any security or product of Ambit or any other service provider before making any investment. You should also take professional / legal /tax advice before making any decision of investing or disinvesting. The investment relating to any products of Ambit may not be suited to all categories of investors. Ambit or Ambit associates may have financial or other business interests that may adversely affect the objectivity of the views contained in this presentation / newsletter / report.

Ambit does not guarantee the future performance or any level of performance relating to any products of Ambit or any other third party service provider. Investment in any product including mutual fund or in the product of third party service provider does not provide any assurance or guarantee that the objectives of the product are specifically achieved. Ambit shall not be liable for any losses that you may suffer on account of any investment or disinvestment decision based on the communication or information or recommendation received from Ambit on any product. Further Ambit shall not be liable for any loss which may have arisen by wrong or misleading instructions given by you whether orally or in writing. The name of the product does not in any manner indicate their prospects or return.

The product ‘Ambit Coffee Can Portfolio’ has been migrated from Ambit Capital Private Limited to Ambit Investments Advisors Private Limited. Hence some of the information in this presentation may belong to the period when this product was managed by Ambit Capital Private Limited.

You may contact your Relationship Manager for any queries.

The performance data for coffee can product between 6th march 2017 - 19th June 2017 represents model portfolio returns. First client was onboarded on 20th June 2017. The performance data for G&C product between 1st June 2016 to 1st April 2018 also includes returns for funds managed for an advisory offshore client. Returns are calculated using TWRR method as prescribed under revised SEBI (Portfolio Managers) Regulations, 2020